Pemeliharaan Terjadwal: Playtech pada 2023-11-30 dari 11.00 PM sampai 2024-05-01 12.29 AM (GMT + 7). Selama waktu ini, Playtech permainan tidak akan tersedia. Kami memohon maaf atas ketidaknyamanan yang mungkin ditimbulkan.

Pemeliharaan Terjadwal: PP Virtual Sports pada 2023-10-13 dari 5.00 PM sampai 2024-06-13 6.30 PM (GMT + 7). Selama waktu ini, PP Virtual Sports permainan tidak akan tersedia. Kami memohon maaf atas ketidaknyamanan yang mungkin ditimbulkan.

Pemeliharaan Terjadwal: Pinnacle pada 2023-08-08 dari 12.45 PM sampai 2024-07-01 12.30 AM (GMT + 7). Selama waktu ini, Pinnacle permainan tidak akan tersedia. Kami memohon maaf atas ketidaknyamanan yang mungkin ditimbulkan.

Pemeliharaan Terjadwal: Crowd Play pada 2023-11-30 dari 7.00 AM sampai 2024-06-07 11.30 PM (GMT + 7). Selama waktu ini, Crowd Play permainan tidak akan tersedia. Kami memohon maaf atas ketidaknyamanan yang mungkin ditimbulkan.

Pemeliharaan Terjadwal: CMD pada 2024-04-19 dari 11.15 AM sampai 4.45 PM (GMT + 7). Selama waktu ini, CMD permainan tidak akan tersedia. Kami memohon maaf atas ketidaknyamanan yang mungkin ditimbulkan.

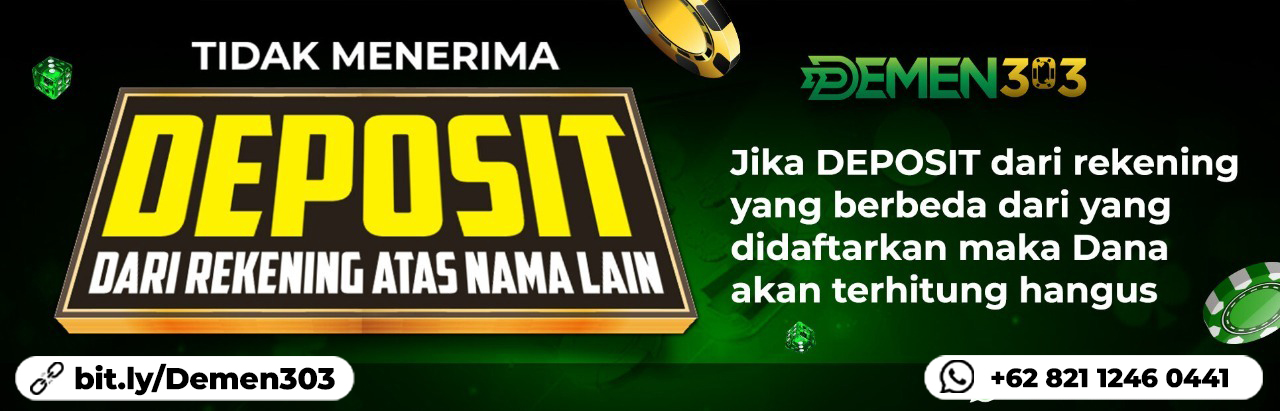

DEMEN303 TIDAK MENERIMA DEPOSIT DARI ATM MINI ATAU EDC

INFORMASI PENTING

Untuk saat ini di karenakan Mesin pencarian Google sedang melakukan update sehingga menyebabkan tidak bisa menemukan penelusuran situs DEMEN303 di google, kami menyarankan untuk menyimpan link Alternatif kami di :